Glossary of Terms

A

ACH – Automated Clearing House

Used by member banks to electronically transfer funds directly from sending bank through the Federal Reserve to the Merchant’s bank.

Acquirer (Acquiring Bank)

A financial institution that maintains the merchant credit card processing relationship and receives all transactions from the merchant to be distributed to the Cardmember Banks.

Agent Bank

Smaller financial institutions that contract to become an issuing and/or acquiring agent of another member bank.

American Express

An organization that issues American Express® cards and acquires transactions, unlike Visa and MasterCard, which are Associations.

Arbitration

The procedure an Acquirer may use to resolve a complaint with a Card Issuer on behalf of the establishment. Use this procedure after a good faith collection attempt has failed.

Associations

MasterCard International, Visa U.S.A., or Visa International, which are licensing regulatory agencies for bankcard activities.

Authorization

Approval by, or on behalf of, the card issuer to validate a transaction for a merchant or another affiliate bank. An authorization indicates only the availability of the cardmember’s credit limit at the time the authorization is requested.

Authorization Approval Code

A number issued to a participating merchant by the Authorization Center that confirms the authorization for a sale or service.

Authorization Center

An organization that electronically communicates a merchant’s request for authorization on Credit Limit credit card transactions to the cardmember’s bank and transmits such authorization to the merchant via electronic equipment or by voice authorization.

Authorized Cardholder

The person who signs for a particular credit card; credit card authorization should be given to only this party.

Auto Close

Automatic capture of transaction in terminal and bank transmission at appointed time.

Available Credit*

The amount of credit available on the cardholder’s credit line after the current balance and outstanding authorizations have been calculated.

Average Ticket

The average dollar amount of a merchant’s credit card transactions.

AVS (address verification system)

In 1996, VISA/MasterCard headquarters introduced a new regulation requiring all businesses who manually key in the majority of their credit card transactions to have a special fraud prevention feature on their credit card processing equipment. This feature is referred to as an address verification system (it checks to see that the billing address and zip code given by the customer matches the credit card). If you opt not to use AVS, VISA and MasterCard will not support your transactions and will charge you an additional fee on those sales.

B (back to top)

BankCard

A Visa or MasterCard card that is widely accepted by merchants as a result of a standard set of rules for the authorization of its use, clearing, and settlement of transactions, used to credit an account for processing a sales transaction. The most common bank card is a credit card.

Bank Identification Number (BIN)

A unique six-digit number assigned by the associations to identify member transactions and accounts for the unique card issuer.

Bankwire

An electronic funds transfer directly from a sending bank, through the Federal Reserve, to the merchant’s bank.

Batch

A collection of credit card transactions saved for submitting at one time, usually each day. Merchants who do not have real-time verification systems must submit their transactions manually through a POS terminal. Batch fees are charged to encourage a merchant to submit his or her transactions at one time, rather than throughout the day.

Business Card

A card issued to corporate clients who provide them to their employees for reimbursable business expenses. The clients can establish individual spending limits for each employee.

C (back to top)

Capture

The process by which the information in a credit card authorization is sent by the credit card processing system to the authorized cardholder’s bank to obtain money for goods and services delivered.

Card Association

A specific credit card company, i.e. Visa, MasterCard, American Express, and Discover.

Card Issuer

Financial organizations authorized by a regulatory organization to issue credit or debit cards to individual cardholders. Also called Cardmember Bank.

Card Reader

Device used to access information from the magnetic stripe of a plastic credit or debit card. The magnetic stripe contains essential cardholder and account information that is necessary for processing transactions.

Cardholder

The authorized user to whom a credit card has been issued. Also referred to as cardmember.

Cash Advance

Cash that is received by a cardholder and appears as a charge on their credit card bill. Cash advances can be distributed by a bank teller or an ATM machine.

Chargeback

A returned transaction resulting from the lack of adherence to the conditions of the Sales Agreement, Association regulations, or the Operating Procedures and the resultant debiting of a merchant account. A chargeback occurs when a card holder disputes a credit card transaction. The card issuer initiates a chargeback against the merchant. The amount of the disputed transaction can be immediately withdrawn from the merchant’s bank account, and the merchant has a limited number days in which to dispute the chargeback with proof of purchase, signature, proof of delivery, etc. A chargeback fee is usually assessed to the merchant on top of the actual transaction. See also retrieval request.

Chargeback Ratios

A comparison between the number of credit card authorizations and the number of chargebacks that one merchant services account acquires.

Check Guarantee Service

A service provided through the merchant’s POS equipment that guarantees payment up to a defined limit, provided the merchant follows proper steps in accepting the check.

Check In

Authorization of card for hotels or rentals.

Check Out

Finalizing sale of authorization from check-in.

Clearing*

The process of exchanging financial transaction details between an acquirer and an issuer to facilitate posting of a cardholder’s account and reconciliation of a customer’s settlement position.

Compliance

Adhering to the Visa and MasterCard regulatory bylaws.

Consumer

The customer who will be purchasing goods or services from you, the merchant – in this case using a credit card.

Corporate Card

A card issued to corporate clients who provide them to their employees for reimbursable business expenses. The clients can establish individual spending limits for each employee.

Credit

A refund or price adjustment given for a previous purchase transaction.

Credit Card

A card that enables the cardholder to purchase goods or services against a line of credit established by the issuer.

Credit Card Authorization

Approval by, or on behalf of, the credit card issuer to validate a credit card transaction for a merchant or another affiliate bank.

Credit Card Processors (or third-party processors)

Merchant services providers that handle the details of processing credit card transactions between merchants, issuing banks, and merchant account providers.

Credit Card Sales Draft

A hardcopy of the contract between the merchant and the authorized cardholder when a credit card transaction has taken place.

Credit Draft

A document evidencing the return of merchandise by a cardmember to a merchant, or other refund made by the merchant to the cardmember.

Credit Limit

The maximum balance that an issuer has approved for the cardholder to carry on a credit card account.

Currency Conversion

The process by which the transaction currency is converted into the currency of settlement or the currency of the issuer for the purpose of facilitating transaction authorization, clearing, and settlement reporting.

D (back to top)

Debit Card

An ATM bankcard that allows a merchant to deduct money directly from a consumer’s bank account. Debit cards issued with a Visa® or MasterCard® logo are accepted by any merchant that also accepts Visa or MasterCard credit cards. For debit card rates, PIN#‘s must be entered at the time of the transaction.

Decline

The response to indicate that a Point of Sale (POS) transaction was not approved.

Deferred Installment and Recurring Billing

The same transaction amount billed to the cardholder at pre-determined timeframes.

Deposit Transaction

The process by which funds are delivered to a merchant services account when a credit card authorization has taken place and goods and services have been delivered.

Dial-Up Terminal

An authorization device, which, like a telephone, dials the authorization center for validation of transactions.

Download

To transfer files or data from one computer to another. To download means “to receive;” to upload means “to transmit.”

E (back to top)

E-commerce

The processing of economic transactions, such as buying and selling, through electronic communication. E-commerce often refers to transactions occurring on the Internet, such as credit card purchases at Web sites. See also Internet commerce.

EDC (electronic data capture)

The use of a POS terminal for validating and submitting credit card transactions to a merchant account provider or other credit card processor. In online credit card processing, software takes the place of the POS terminal.

EFT (electronic funds transfer)

The movement of monetary funds from one source to another utilizing electronic transmission over various telecommunications’ networks. Transfer of money initiated through electronic terminal, automated teller machine, computer, telephone, or magnetic tape. Since the late 1990s, this increasingly includes transfer initiated via the Web. The term also applies to credit card and automated bill payments.

Electronic Benefits Transfer (EBT)

Electronic acceptance of government benefits (e.g., food stamps and/or cash).

Electronic Deposit

The way in which the credit card association sends money to the merchant account when a credit card authorization has taken place and goods and services have been delivered.

Electronic Draft Capture (EDC)

A process which allows the merchant’s dial-up terminal to receive authorization and capture transactions, and electronically transmit them to i3 Verticals for processing. This eliminates the need to submit paper for processing.

Encryption

A method of coding data, using an algorithm, to protect it from unauthorized access. There are many types of data encryption, and they are the basis of network security.

Expected Monthly Volume

The amount of money a merchant plans to process in credit card transactions in one month.

Expiration Date

The date embossed on the credit card beyond which the card is not acceptable by the establishment at the Point Of Sale (POS).

F (back to top)

Factoring

The purchase of debts owed, or “accounts receivable,” in exchange for immediate payment at a discount. In e-commerce, the term is often applied to ISOs that offer to process credit card transactions through their own merchant account rather than through an account established by the merchant, in exchange for a percentage of the transaction or other fee. Factoring of credit card debt is illegal.

Fleet Card

A card issued to corporations for control and tracking of fleet purchases on a single card.

Floor Limit

The minimum dollar amount established for a single unauthorized transaction. Authorize transactions exceeding the floor limit. A zero floor limit requires an authorization on all transactions.

Fund Turn-Around Time

Time it takes to receive deposits after a batch is transmitted to a merchant’s bank.

G (back to top)

Gateway

A software device that connects a merchant to their processor. It translates between protocols so that computers on the connected networks can exchange transaction data.

Gift Card

A magnetic-stripe or smart (chip) card that replaces traditional paper gift certificates that are most often used in retail, restaurant and lodging establishments.

H (back to top)

Help Desk

Customer service agents that service merchants with technical problems; provided by the network/processor.

Holdback/Reserve

A portion of the revenue from a merchant’s credit card transactions held in reserve by the merchant account provider to cover possible disputed charges, chargeback fees, and other expenses. After a predetermined time, holdbacks are turned over to the merchant.

Host Capture

Processor captures transactions and sends them to merchant’s bank instead of Terminal Capture.

I (back to top)

ICA Number

A distinctive four-digit identification number assigned by MasterCard to identify a member or processing endpoint.

Imprint

An imprint of a customer’s credit card can be electronic (swiping the card through a credit card terminal) or manual (taking a physical impression of the credit card by utilizing a card imprinter). Either of these two methods is required to prove the cardholder’s credit card was present.

Initialize or Partial Download

Short download needed to be done at merchant’s terminal to complete and pick up any changes made to the software.

Interchange

The exchange of transaction data between acquirers and issuers through the associations.

Interchange Compliance

A process to ensure that the appropriate interchange rate is applied to a transaction in accordance with association requirements.

Internet Software

The product that sets up a system for a merchant account to do credit card processing online.

ISO/MSP

Independent Sales Organization; independent sales group representing Visa & MasterCard Processors.

J (back to top)

Sorry, no matches were found.

K (back to top)

Keyed Credit Card

The credit card is not present and the merchant punches in the information from the credit card into the credit card terminal.

L (back to top)

Leased Line

A private Point-to-Point communications link, originating and terminating at specific points.

M (back to top)

Magnetic Stripe

A stripe of magnetic information affixed to the back of a plastic credit or debit card. The magnetic stripe contains essential cardmember and account information.

Mail Order/Telephone Order (MO/TO)

Refers to direct marketing (card not present transactions).

Manual Imprinter

A piece of credit card processing equipment in which the merchant physically rather than electronically imprints information off a consumer’s credit card.

Manual Sale

Card won’t swipe due to bad magnetic strip or bad magnetic strip reader or card taken over phone which forces merchant to key in credit card # by hand.

MasterCard

An association of banks that governs the issuing and acquiring of MasterCard® transactions.

Media Retrieval Requests

Media retrieval is the process of obtaining paper documents from a centralized location. There are two types of media retrieval requests that can be obtained: 1) requests for sales drafts from merchants and 2) requests for documentation in defense of the chargeback from card issuers. Merchants must fulfill media within 12 days of receipt. If the media is fulfilled after 12 days of receipt, the status is fulfilled late. If the media is not fulfilled at all, the status is expired.

Merchant

Store owner or seller of products.

Merchant #

A series or group of numbers that numerically identifies each merchant account to the credit card processing company or merchant bank for accounting and billing purposes.

Merchant Account

Account needed for credit card processing.

Merchant Agreement

The initial correspondence and contract between the merchant and the credit card processing company; when this agreement is approved, a merchant services account is set up.

Merchant Bank

A bank that holds a merchant account. After a consumer buys a product using a credit card, the merchant bank places funds into a merchant account in exchange for the right to collect on the debt owed by a consumer.

Merchant Category Code (MCC)

A code assigned by an Acquirer to identify a merchant’s type or mode of business and the merchandise sold.

Merchant ID

A series or group of numbers that numerically identifies each merchant account to the credit card processing company or merchant bank for accounting and billing purposes.

Merchant Services Provider

A bank, ISO, or other firm that provides services for processing financial transactions, usually credit card sales.

Merchant Statement

Summarizes merchant’s credit card activity and fees accrued for a given month. Usually sent to merchants at the end of the first week of the following month.

N (back to top)

Network

The software that provides the application for the terminal that processes the credit card.

Non-Bankcard Authorization

Authorization of T+E cards.

O (back to top)

Offline Debit

Offline debit transactions take place using the dual message credit card processing method in which the authorization occurs at the time of the transaction using one message, and the transaction is settled later using another message. These transactions do not require a PIN (Personal Identification Number), but do require the cardholder’s signature. This transaction is processed like a credit card with the posting to the cardholder’s account within a few days of the transaction occurrence. These are often referred to as ‘check card’ or ‘debit card’ transactions.

Offline Entry

Sale inputted to terminal using a pre-obtained authorization code.

Online Debit

An online debit transaction occurs in a single message format that allows the transactions to be completely settled from an authorization request. This method requires a cardholder to enter their PIN (Personal Identification Number). The transaction must be approved online by requesting authorization from the financial institution. If the transaction is approved, funds are withdrawn from the cardholder’s account at the time of the transaction. The funds for the transaction are guaranteed to the merchant.

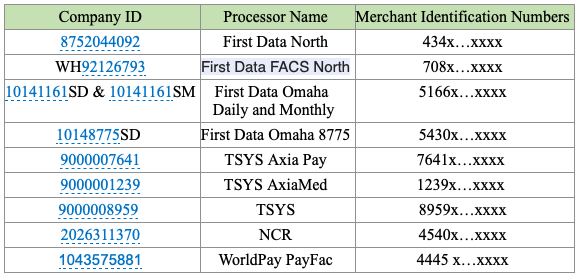

Originator ID

An Originator ID is a numeric value used by the ACH network to identify the origin of a transaction.

Merchants designate the bank accounts to be used for payment processing activity on ACH authorization forms with the original merchant application or through subsequent forms if changed after the approval date. Many corporations establish filters with their banks that only allow ACH debits from authorized originating entities. Banks use Company IDs, also known as Originator IDs, to filter for authorized originators. If your company has filters set up with their banks, click here to view the table to provide your bank the i3 Verticals Company IDs. This will avoid unnecessary returns and return item fees.

{kind=link}

P (back to top)

Payment Gateway

The code that transmits a customer’s order to and from a merchant’s bank’s transaction-authorizing agent.

PIN (personal identification number)

An alphanumeric or numeric code used to verify the identity of an individual attempting to use a credit card, debit card, or other account.

Pin Pad

Used to enter PIN for a debit transaction; usually a separate piece of equipment connected to the terminal.

Point Of Sale (POS)

The point at which a product is purchased and delivered.

Point of Sale Terminal

A device placed in a merchant location which is connected to the processor’s system via telephone/leased lines and is designed to authorize, record, and settle data by electronic means for all sales transactions with the merchant processor.

Primary Account Number (PAN)

The cardholder’s account number to which transactions are to be charged.

Private Label

A credit card issued by merchants, to be used only in their stores.

Processor

A transaction processor, distinct from the bank, that processes data from the credit card transactions and then distributes funds from the merchant’s bank account.

Q (back to top)

Quasi-Cash Transaction

A transaction representing a merchant’s sale of items that are directly convertible to cash, such as: gaming chips, money orders, opening deposits, wire transfer money orders, etc.

R (back to top)

Real Time Credit Card Processing

Online verification and processing of credit card transaction authorizations.

Receipt

A hard copy (paper) document recording a transaction. The receipt usually includes date, merchant name/location, account number, amount, reference number, and signature, if the cardholder is present at the time of the transaction.

Reconciliation

The process of checking the amount processed against the amount funded to a merchant’s checking account. Also to make compatible or consistent, with regards to numbers and accounting.

Recurring Transaction

Items that are charged periodically to the customer, for ongoing services.

Referral

The message received from an issuing bank when an attempt for authorization requires a call to the Voice Authorization Center or Voice Response Unit (VRU).

Representment

A transaction presented to the issuer by the acquirer when the establishment requests a reversal of a chargeback.

Reserve Account

Set up by the credit card processing company to protect themselves in case of losses due to chargebacks or if the merchant defaults on their merchant account. See holdback.

Retrieval Request

A request to a merchant for either a legible copy or an original sales record.

Reversal

A request by the establishment to represent a chargeback to the card issuer.

S (back to top)

Sales Draft

A document used as proof of purchase for goods or services by a cardholder.

Secure Electronic Transaction (SET)

A protocol developed by MasterCard International, Visa International and others to protect the security of credit card transactions conducted over the Internet.

Settle Batch

The act by which the merchant sends all of the credit card processing transactions for a particular day to the credit card processor.

Settlement

The process by which members exchange financial data and value resulting from sales transactions, cash disbursements, or merchandise credits, which are ultimately billed to the cardholder’s account so that all parties in a transaction are paid for their goods or services.

Shopping Cart Program

A software package that runs as part of a Web site to collect and record purchasing decisions by a visitor. Shopping cart programs are stored on Web servers.

SIC (Standard Industry Classification) Code

A number assigned by an Acquirer to identify a merchant’s business type (also known as MCC- Merchant Category Code).

Signature Capture

Electronic capture of the signature of a cardholder, which eliminates the need for paper storage/retrieval.

Smart Cards

Payment cards with built-in computer chips that allow them to manipulate and retain data. Monetary value can be transferred from a bank account to the smart card’s chip via a smart card device that writes to the chip. Unlike a credit card, a smart card can only spend out the dollar amount its owner has already put into the card account.

Split Dial Authorization

A process which allows the authorization device to dial directly to different card processors (e.g., American Express) for authorization. In this instance, the merchant cannot be both EDC and Split Dial.

Split Dial/Capture

Process which allows the authorization terminal to dial directly to different card processors (e.g., American Express) for Authorization and Electronic Draft Capture.

Submission

The process of sending batch deposits to the Acquirer for processing.

Swiped Cards

Credit or debit cards that were magnetic stripe read (processed via the card reader).

T (back to top)

T+E Card

Travel and Entertainment cards such as American Express, Discover, Diners, JCB (rates are determined by T+E Card company).

Terminal

Machine that processes credit cards (ex. Verifone Tranz 330 or Hypercom T77).

Terminal Application

Type of software program used to run terminal (ex. Restaurant, Retail, Hotel, MOTO).

Terminal ID

A series or group of numbers that numerically identifies a specific piece of credit card processing equipment to the credit card processor.

Tip

Customer tip added to sale after sale has been entered and authorized by terminal.

Tip Assist Program

Restaurant application that automatically calculates 10%, 15%, 20%, etc. of sales amount.

Transaction

A credit card sale or refund between the cardholder and merchant, or the processing of the exchange by the Acquirer.

Transit/Routing #

Nine digit number identifying a particular bank.

U (back to top)

Underwriting

To assume financial risk for a merchant’s credit card processing by a bank that is a member of the card association.

V (back to top)

V#

Visanet’s identifier for Terminal # for each unique processing terminal.

Valid Date

The date embossed by the card issuer on the credit card. An establishment cannot accept a card for payment of goods or services prior to this date.

VAR

Value Added Reseller; provides the software to run POS Systems.

V-Code or CVVC

Additional 3 digits on the back of bank cards used in efforts of fraud patrol.

Virtual Terminal

On-line terminal used to process credit cards.

Visa

An association of banks that governs the issuing and acquiring of Visa credit card transactions.

Voice Authorization

When a merchant calls to obtain a verbal credit card authorization rather than using a terminal or credit card software to obtain the authorization. The merchant must, in addition to the voice authorization, submit the credit card information via terminal or software to close out the transaction and transfer the funds to the merchant’s bank account. This is performed by manually entering the transaction information into the terminal or software.

Voice Response Unit (VRU)

Technology employed at various call centers that handle simple customer requests (e.g., account balance inquiries) that do not require personal assistance. Ordinarily, customers are provided with instructions and they respond by pushing keys on a touch-tone telephone keypad.

Void

Deleting a transaction in a batch due to error or return prior to submission or settlement.

W (back to top)

Sorry, no matches were found.

X (back to top)

Sorry, no matches were found.

Y (back to top)

Sorry, no matches were found.

Z (back to top)

Sorry, no matches were found.

# (back to top)

3rd Party Processor

Company who sets up and manages merchant on behalf of Visa & MasterCard.